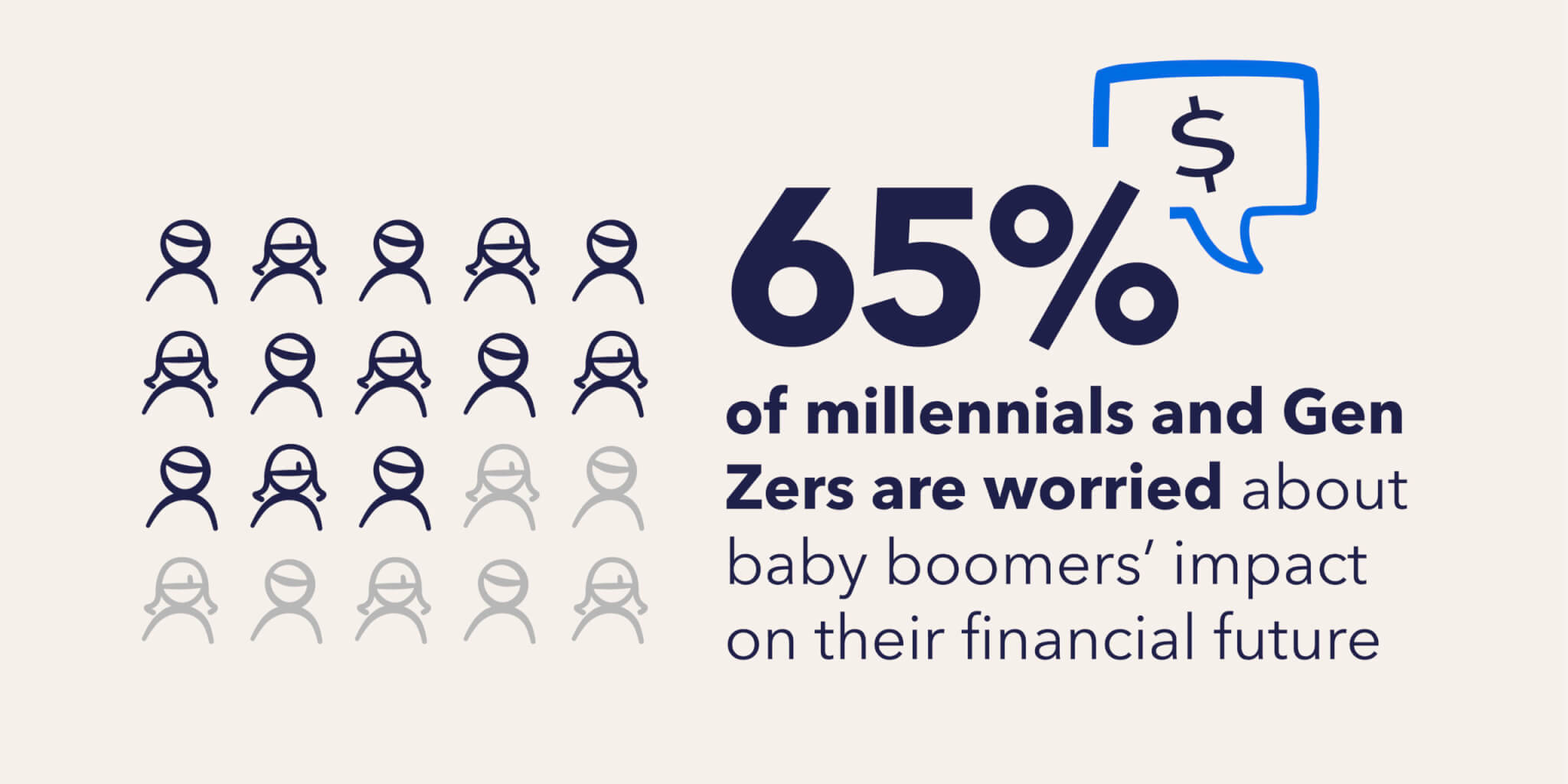

NEW YORK — Sixty-five % of millennials and Gen Zers are anxious about child boomers’ affect on their monetary future, in line with new analysis. A survey of two,000 U.S. adults evenly break up by technology seemed on the variations between their monetary experiences. Outcomes present that though youthful generations are anxious about their elders getting of their method, unhealthy cash habits are literally widespread amongst People of all ages.

Simply 27 % fee their money-saving habits as “glorious.” Despite the fact that respondents have some good habits, most admit they make poor cash selections typically (62%).

The survey, carried out by OnePoll for National Debt Relief, finds that among the most typical bad money habits embody writing off small purchases as insignificant (43%), playing (39%), and utilizing bank cards to pay payments (33%). Respondents say their cash habits are impressed by their dad and mom (48%).

Whether or not these classes have been sound may very well be up for debate as greater than half of People have been in debt in some unspecified time in the future (51%) and 42 % are presently experiencing financial difficulties. In gentle of those monetary struggles, many wish to destigmatize the concept that going through unmanageable debt is “shameful” or embarrassing (36%).

Monetary blame recreation

Whereas millennials have been discovered to take essentially the most accountability for his or her habits (71%), a majority of them who’re going through monetary difficulties nonetheless imagine their troubles are penalties of child boomers’ financial decisions (75%). But, child boomers are essentially the most immune to believing that they make poor money decisions (27%). Of all those that are presently in debt, boomers have the fewest variety of respondents who fall into this class (45%).

“This survey confirms one thing many people really feel, however don’t all the time speak about: managing money could be powerful, and all of us make errors,” says chief consumer operations officer at Nationwide Debt Aid, Natalia Brown, in a press release. “There’s lots of guilt and disgrace individuals really feel once they’re in debt and that should change. The information exhibits that almost all of us face challenges with cash and that none of us are alone in that.”

Millennials additionally report having essentially the most details about create good financial habits (74%) and utilizing it (45%), whereas boomers say they want extra (30%). Gen Z respondents admittedly have the instruments and data they want however haven’t used them (40%).

Practically 1 / 4 of all respondents really feel like they want higher data about develop good monetary habits (23%). This can be why 37 % look as much as business professionals and 26 % take heed to podcasts or radio exhibits. Curiously, influencers have the least monetary affect (16%).

Gen Z, notably, looks like they’ve rather a lot to be taught from earlier generations and would take their elders’ recommendation critically (47%). A very powerful monetary lesson that Gen Z and millennials have realized as they’ve aged is successfully handle and cut back debt (49% and 61% respectively).

Some recommendation older generations could also be eager to supply the youthful crowd is to have an emergency savings fund (61%) and to save lots of and invest earlier (53%).

Though they provide good recommendation, youthful generations expressed concern about paying for others’ errors sooner or later. Between Gen X and child boomers, the previous are practically thrice as more likely to acknowledge that their technology’s monetary selections can have a big affect on the way forward for youthful generations (23% vs. 9%).

Simply 35 % of older respondents suppose their technology will go away the economic system in a very good state for future generations.

“There are various instruments and sources out there to assist individuals be taught and undertake higher cash habits,” provides Brown. “No matter technology, financial literacy and schooling is necessary for securing a more healthy monetary future. By empowering ourselves with sensible cash habits, we’re not simply securing our monetary wellbeing, however fostering a tradition of fiscal accountability that can resonate for generations to come back.”

Survey methodology:

This random double-opt-in survey of two,000 normal inhabitants People break up evenly by technology was commissioned by Nationwide Debt Aid between August 4 and August 8, 2023. It was carried out by market analysis firm OnePoll, whose group members are members of the Market Research Society and have company membership to the American Affiliation for Public Opinion Analysis (AAPOR) and the European Society for Opinion and Advertising Analysis (ESOMAR).